The US government recently hit its $31.5 trillion debt limit after years of careening baseline spending on entitlements combined with emergency COVID-19 spending in the last few years to produce record-busting deficits. The new Republican majority in the House of Representatives, elected largely on economic concerns like inflation and runaway spending, now faces an obstinate Senate and White House. A showdown appears likely as does the ritual brow-beating of all those who object to simply raising the debt limit “without conditions,” as President Biden demands.

To those who will inevitably cry, “Don’t use the debt ceiling as a negotiating tool!” over the coming weeks and months, it should be pointed out that it is the only tool that has been even remotely effective at taming Congress’s appetite for spending. In the same way that an intervention is only possible when a drug addict is in crisis, debt limit negotiations are the only context in which Uncle Sam has accepted even modest constraints on government spending in recent decades.

Conservatives and libertarians rightly decry the rapidly-expanding national debt as an embarrassment, a threat to the nation, a root cause of inflation (as the Federal Reserve must expand its balance sheet to purchase the Treasuries that finance these huge deficits, as happened most clearly in the pandemic’s peak), and a promise of higher future taxes. While all these are accurate observations, one effect of massive government spending and deficits is often overlooked in the standard conservative critique: the forgone private investment of capital and therefore forgone economic growth, often termed the “crowding out effect.”

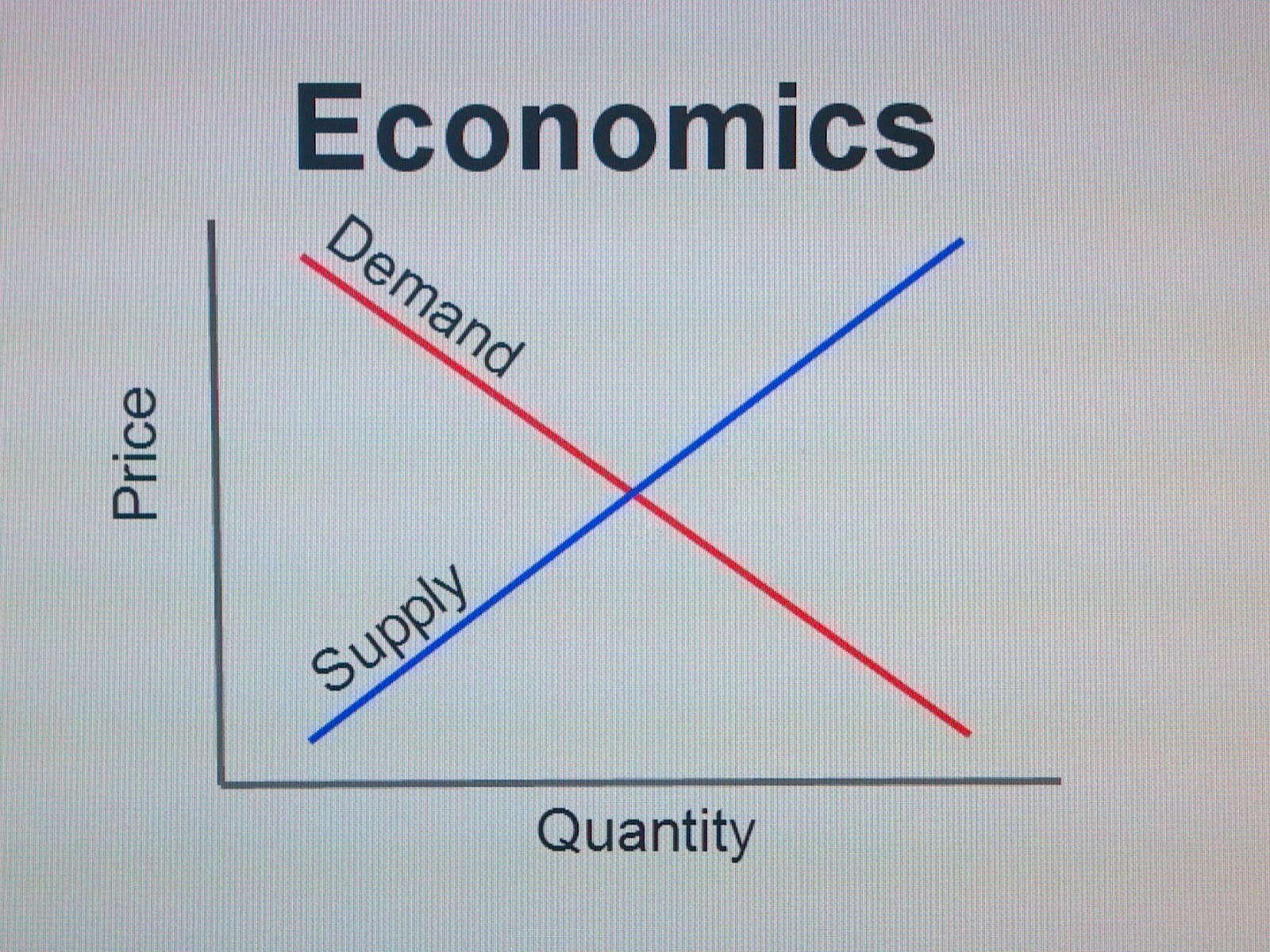

The basic idea is that there exists a total sum of money, or financial capital, that individual and institutional investors are willing to loan out or invest. Most economists call this the “loanable funds market.” The supply of loans, as with any supply curve, slopes upward and to the right. In other words, as the interest rate (the price of a loan) rises, more people will be eager to supply loans. In contrast, the demand for loanable funds slopes, like a normal demand curve, downward and to the right. That is, as the interest rate goes down, more people are interested in borrowing money. Just think of any normal supply-demand graph, but with the good in question being a loan rather than a physical good or a service, and the vertical axis labeled “interest rate” rather than “price,” as in other markets.

The demand for loanable funds is a function of how much capital investment businesses need (which is itself a function of how profitable those capital investments are), what quantity of money consumers need for purchases like homes and new vehicles, and how much money the government needs to borrow. In a game where the total supply of loanable funds per year is set, say at $5 trillion, every $1 trillion the government runs up in deficits is $1 trillion less available for private investment in the innovations that improve quality of life, bring us new medicines, and create new jobs.

Increased government deficits shift the demand for loanable funds to the right. As any student of elementary economics knows, this increases the price, or in this case, the nominal interest rate. Many private sector projects that make sense at 4 percent interest are no longer acted upon if the government runs such a large deficit that the interest rate must increase to 7 percent for investors to shell out the cash necessary to finance that deficit. Increasing the supply of loanable funds through monetary expansion, as happened in the COVID pandemic with breathtaking speed, can temporarily hide this effect. However, this spurs inflation that reduces real returns and hampers economic growth (the stock market’s dismal returns since runaway inflation started in late 2021 is one example of this result).

In contrast to the Keynesian “money multiplier” theory, which insists that government spending stimulates the economy by circulating money via transfer payments that otherwise would have remained in savings and uncirculated, savings in nearly all developed countries are not locked away gathering moths and rust, but invested. Of every dollar put in the bank, more than 90 percent is invested in loans for commercial enterprises, in home loans, and in bonds, and this doesn’t account for the fact that a larger and larger share of surplus savings in the United States are not in the traditional banking system, but in brokerage accounts, 401(k)s, and elsewhere.

Government spending does not multiply the economic power of money, it diminishes it. If the opposite were true, Cuba, North Korea, and Venezuela would be among the wealthiest nations on the planet, since nearly all economic activity is facilitated through government spending in those nations. That they are not, but that nations with relatively free markets such as the United States, Singapore, the United Kingdom, and Japan punch above their weight economically suggests that private investment in the innovations and technologies of tomorrow everywhere and always beats government transfer payments in facilitating economic growth.

Every dollar the government must borrow is a dollar not available for private businesses or individuals to borrow, and that reduces future economic growth and job creation. With America’s debt now hovering near 125 percent of GDP (before netting for debt held by government entities) and deficits topping $1 trillion yearly as far as the eye can see, we can no longer ignore this drag on the American economy.

Nathan J. Richendollar

Nathan Richendollar is a summa cum laude economics and politics graduate of Washington and Lee University in Lexington, VA. He lives in Southwest Missouri and works in the financial sector.

This article was originally published on FEE.org. Read the original article.

{kind=link}